Supported by investor optimism and fundamentals, U.S. stocks continue to hit new highs, and three important indicators suggest that the bull market in U.S. stocks will not dissipate anytime soon.

After last week’s election, brokers said that there was a significant increase in trading volume during extended trading hours. Robinhood (NASDAQ:HOOD) reported that its night trading volume has soared to 11 times its usual level since the launch of 24-hour trading last year.

Similarly, Interactive Brokers (NASDAQ:IBKR) set a record with 349,910 trades executed, including 188168 U.S. equities and 161742 derivatives.

Options trading volume also exceeded $160 billion, a record high, and confidence was strong across sectors. A strong combination of positive seasonal trends, election results, and new market leaders supported the continued rally in U.S. equities.

There are many factors driving the strength of U.S. stocks, and there are three key reasons why there is still plenty of room for upside in the future:

U.S. stocks tend to be strong after elections

History shows that markets tend to see a rally after a presidential election, and this year was no exception.

The Dow Jones Industrial Average, S&P 500, Nasdaq and Russell 2000 all rose sharply after the election.

On average, the Dow Jones Industrial Average rose by 2.38%, the S&P 500 by 2.03%, the NASDAQ by 1.50%, and the Russell 2000 by 4.93%.

Historically, strong post-election performance has supported this prospect, with a nine-in-ten probability of a rise in stocks in the year after the election, with an average increase of 15.2%.

Technology stocks will help the Dow Jones rise

Technology stocks continue to dominate the market, and the latest correction to the Dow Jones underscores the growing importance of the technology sector. The inclusion of Nvidia (NASDAQ:NVDA) in the Dow Jones index, replacing Intel (NASDAQ:INTC), marks a major shift.

Nvidia stock price chart, source: Investing.com

Today, the Dow Jones is led by tech giants such as Nvidia, Apple (NASDAQ:AAPL) and Microsoft (NASDAQ:MSFT) as a highly tech-weighted index. Investors are betting on continued strength in the tech sector, which has historically been a key driver of market growth.

Nvidia, in particular, has performed particularly well this year. Nvidia will soon report results, which are expected to be strong, which is expected to further boost investor optimism.

The Big Seven Daily

The market is resilient, thanks to strong consumer confidence, which is currently at an all-time high.

The latest Conference Board survey showed that confidence that stock prices will continue to rise through 2025 is stronger than ever, and traders have built the largest long positions in U.S. stock futures in history.

The optimistic outlook suggests that investors are not just buying with the trend, but also betting on continued growth in the future.

In terms of investor sentiment, the latest American Association of Individual Investors (AAII) survey showed that bullish sentiment has risen, rising 2.1 percentage points to 41.5%, well above the historical average of 37.5%.

At the same time, bearish sentiment fell by 3.3 percentage points to 27.6%, still below the long-term average of 31%. Reflecting an overall optimistic outlook, investors are confident about the market direction at the end of the year.

With the combination of investor confidence, historical trends, and the dominance of the technology sector, the bull market in U.S. stocks shows no signs of dissipating.

The report released by the US Department of Labor on Friday showed that non farm payroll employment increased by 142000 in August, significantly higher than July’s 89000, but lower than market expectations of 161000; The unemployment rate for the month decreased slightly by 0.1 percentage points to 4.2%, which is in line with expectations and the first decline in five months.

The Ministry of Labor also significantly revised down the employment data for the months of June and July. Among them, the number of non-agricultural employment in July decreased by 25000 to 89000, and the number of employment in June decreased by 61000 to 118000.

The addition of new job opportunities fell short of expectations, which means that the slowdown in economic growth may exceed expectations. Due to this concern, the US stock market fell across the board on Friday, and the technology sector suffered a bloodbath. The Dow Jones Industrial Average closed down 410.34 points, or 1.01%, at 40345.41 points; The S&P 500 index fell 1.73% to 5408.42 points; The Nasdaq index fell 2.55% to 16690.83 points.

Based on recent speeches by Federal Reserve officials, there is little doubt that the Fed will initiate its first interest rate cut in four and a half years at its policy meeting on September 17-18. However, it is uncertain whether the rate cut will be 25 basis points or 50 basis points.

After the release of the employment report, the futures market once tended to lower interest rates by 50 basis points, but then fell back to 25 basis points. On Saturday morning Beijing time, data from the Chicago Mercantile Exchange’s Federal Reserve Watch tool showed a 69% probability of a 25 basis point rate cut in September and a 31% probability of a 50 basis point rate cut; The probability of a cumulative interest rate cut of at least 100 basis points within the year is 89.9%.

Two Federal Reserve officials gave speeches after the release of the employment report. The data we have seen recently indicates that the labor market is continuing to weaken, but not worsening, and this judgment is crucial for the decisions we are about to make, “said Federal Reserve Governor Christopher Waller. Federal Reserve Board members are members of the Federal Open Market Committee (FOMC), commonly known as the “vote committee”, who have voting rights on issues such as interest rate hikes/cuts.

Waller did not explicitly mention a 25 or 50 basis point rate cut, but hinted that he tends to support a 25 basis point rate cut first. However, he later stated that if new data shows that the labor market is deteriorating, he would also be open to a significant interest rate cut.

The other official speaking was John Williams, the President of the New York Federal Reserve and one of the 12 members of the FOMC. Williams repeated in his speech the remarks made by Federal Reserve Chairman Jerome Powell at the Jackson Hole Central Bank meeting last month, stating that it was time to relax monetary policy, but did not comment on the magnitude of the rate cut.

From the previous interest rate adjustments by the Federal Reserve, 25 basis points is the norm, while adjustments of 50 basis points or greater are generally used in special or emergency situations. For example, in March 2020, at the beginning of the COVID-19, the Federal Reserve announced to cut the federal benchmark interest rate by 100 basis points to 0-0.25%. In 2022-2023, in response to rare high inflation, the Federal Reserve has raised interest rates by 50 or even 75 basis points multiple times, pushing the federal benchmark interest rate from near zero to the range of 5.25% -5.50%.

James Bullard, Dean of the Purdue University School of Business and former President of the St. Louis Fed, stated that he believes there will be a 25 basis point rate cut in September as the August employment data is roughly in line with expectations. Although the Federal Reserve may currently be in a somewhat unfavorable position, I believe it is not yet at the point where it needs to cut interest rates by 50 basis points

But many analysts have also warned that the labor market is cooling significantly, and if the Federal Reserve cuts interest rates too slowly, this situation will further worsen. Jason Price, head of investment strategy and research at wealth management firm Glenmede, said, “The labor market has not yet bottomed out, but the Federal Reserve has enough concerns to seriously consider a 50 basis point rate cut later this month

Seema Shah, Chief Global Strategist at Principal Asset Management, stated that for the Federal Reserve, a 50 basis point rate cut could reignite inflationary pressures, while a 25 basis point rate cut could trigger the risk of an economic recession. In such cases, the key is to determine which option carries greater risk. In a situation where inflation pressure is not high, there is no reason not to act cautiously and adopt a larger interest rate cut, “Shah said.

In addition, prior to the release of the employment report, renowned American economist and Nobel laureate Joseph Stiglitz stated at the Ambrosetti Annual Economic Forum held in Italy that regardless of the performance of the August employment data, the Federal Reserve should cut interest rates by 50 basis points at this month’s policy meeting. He accused the Federal Reserve of “going too far and too fast” in tightening monetary policy, which has made the inflation problem worse.

Stiglitz said that it was a mistake for the Federal Reserve to keep the benchmark interest rate close to zero for a long time after 2008. But later on, they began to raise interest rates significantly, which not only did not benefit the economy much, but may also exacerbate inflation

He pointed out that if we carefully study the sources of inflation, we will find that housing costs are an important factor. A significant increase in interest rates will lead to an increase in construction costs for real estate developers and a rise in purchasing costs for homebuyers, which goes against the goal of solving the housing shortage problem.

A group of people eagerly arranged to meet at the bar, staring intently at the TV screen next to the table. And what is playing on the screen is not an exciting sports event, but the financial report and performance of a listed company

This scene happened in a bar near Madison Square Park in Manhattan, New York: dozens of investors gathered together, just waiting for the exclusive “Super Bowl” moment of the financial market – the disclosure of Nvidia’s Q2 financial report.

They were drinking beer and red wine while watching CNBC’s live broadcast, and as Nvidia’s financial report was released, they exchanged their respective holdings. Some people expressed that they hope today can be lively and drive the stock price to soar; Others expressed that they only came to enjoy the show, establish connections, or boast about attending the financial report “observation meeting” for the first time in their lives.

As time passed, these investors cheered and cheered during the countdown phase before the release of the financial report, while booing was heard when the stock price fell after hours.

Finally, the gathering came to an end quickly. At 5pm local time, as the stock price fell, the number of people gradually decreased.

Did Nvidia’s latest financial report disappoint them? Perhaps it is.

The graphics chip manufacturer, which has become a cultural phenomenon and symbol of AI frenzy, announced on Wednesday that Nvidia’s Q2 revenue and profit exceeded Wall Street’s expectations, but the growth rate of performance has slowed down compared to recent quarters. At the same time, the Q3 revenue outlook was higher than analysts’ average expectations, but did not exceed those most optimistic expectations, which led to a sharp drop of 8% in its stock price after hours.

Marty Jaramillo, sports injury data analyst at CBS Sports, commented on the stock price trend of Nvidia that day, saying, “This is a bit disappointing. On its own, Nvidia still hit a ‘home run’ today, but they have hit many ‘home runs’ in the past few quarters

He said that people’s expectations may be too high.

In fact, not everyone was optimistic about Nvidia’s performance before this gathering. Some attendees even expressed that they believe the emergence of similar gatherings is itself a signal of market peak. It’s like when everyone is talking about seeking to buy stocks, it’s often the most dangerous moment

The most important stock on Earth

The quarterly financial performance report is a mandatory disclosure for US listed companies. In the past, financial reports rarely attracted such great attention from the outside world, but it is clear that for the entire US market and even the global market, Nvidia is no longer an ordinary company

It is the best performing stock in the S&P 500 index this year, having more than doubled since 2023 and more than doubled since 2024. Nvidia’s market value has currently exceeded $3 trillion, ranking second in the world, and has a huge impact on the direction of the US benchmark stock index. It is also a key indicator that may directly affect investor trading sentiment.

Since entering this week, some market observers have been speculating whether the comments made by NVIDIA CEO Huang Renxun on the quarterly earnings conference call will have a more significant impact on the market than the speech made by Federal Reserve Chairman Powell at the Jackson Hole annual meeting last week. At last week’s central bank annual meeting, Powell released a significant signal that the Federal Reserve is about to cut interest rates.

According to data from Deutsche Bank, in the first few quarters, the market reaction triggered by Nvidia’s financial report was comparable to the market reaction after the release of heavyweight macroeconomic reports such as monthly non farm payroll reports or inflation data in the United States. It’s no wonder that before the release of the financial report, many traders were betting that Nvidia’s market value would fluctuate by around $300 billion after the report was released.

Michael Antonelli, Managing Director of investment firm Baird, said, “People are pushing the entire US stock market onto Nvidia’s shoulders. It seems absurd.”

But investors who have experienced the market trend over the past year are clearly aware, and such descriptions are not even exaggerated. Among retail investors in the United States, Nvidia’s name has almost been placed in everyone’s watchlist for self selected stocks. For some amateur investors who hold NVIDIA, the skyrocketing stock price in the past few years has allowed them to retire early, travel, repay debts, or save money to buy a house.

FactSet data shows that individual investors and small asset management companies currently hold approximately 30% of Nvidia’s stock.

People’s pursuit of Nvidia has even ignited the surrounding area. A hat with the name “NVIDIA Day” printed on it is priced at up to $33, which has almost become a symbol of people’s enthusiasm for NVIDIA’s financial report.

47 year old entrepreneur David Osterweil said he first bought Nvidia stock in 2020 and has been holding the stock ever since, regularly reducing some positions to lock in profits. He said that the profits from investing in Nvidia are helping him pay for his son’s coming of age gift.

He is not worried about Nvidia’s financial performance on Wednesday and stated that the expectations before the report was released were already high. I think over time, this will be a slow and steady climb. This (Nvidia) is still largely worth holding for the long term

Da Mo summarized this financial report and market reaction as the result of a bull market case, but the price action of a bear market. Bank of America Merrill Lynch stated that Nvidia has unique growth opportunities and strong execution capabilities, Goldman Sachs holds a constructive attitude towards Nvidia’s data center prospects, and Barclays believes that key long-term issues have been resolved.

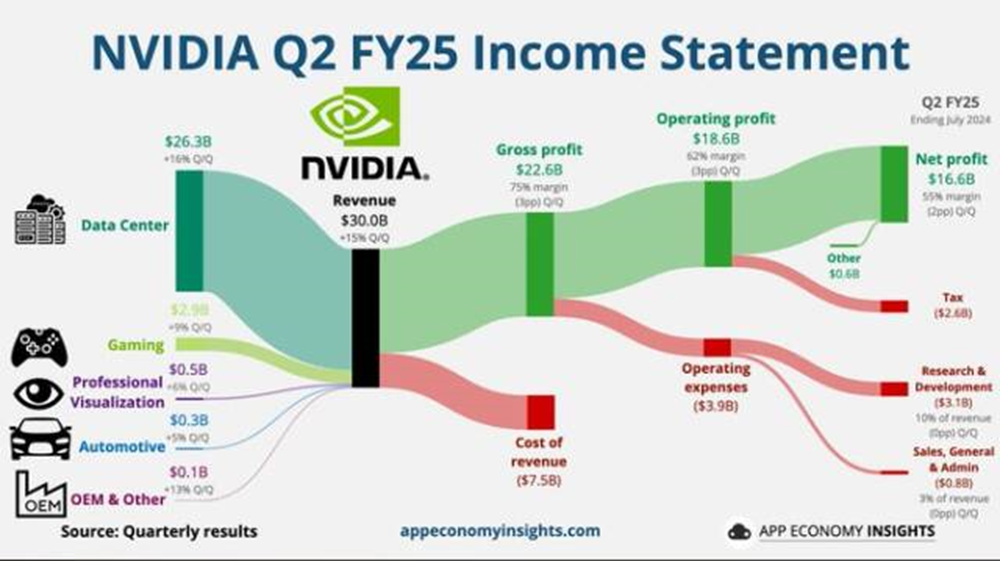

The financial report released by NVIDIA shows that its revenue for the second quarter of 2025 (the second quarter of 2024) increased by 1.2 times year-on-year to $30 billion, reaching the highest market expectation range ($29 billion to $30 billion). The revenue guidance for the third quarter (Q3) is $32.5 billion, which is in the middle of the expected range ($32 billion to $33 billion).

Although revenue continued to grow rapidly, the guidance did not meet Wall Street’s most optimistic expectations, and coupled with the delayed delivery of the so-called “strongest chip in history” Blackwell, Nvidia’s stock price fell 8% after the US stock market closed.

After the heavyweight financial report was released, Wall Street analysts summarized it one after another. To summarize with Morgan Stanley’s review: Nvidia’s performance in the second quarter was excellent, but it was far from enough. The market’s expectations for this top student were too high.

Wall Street believes that there are two major concerns in the market at present: when Blackwell will become the new engine for Nvidia’s performance growth, and whether the demand for AI chips can maintain high growth.

Regarding the first question, Nvidia stated during the conference call that with Blackwell starting mass production in the fourth quarter, it is expected to generate billions of dollars in revenue, but did not answer whether the billions of dollars in revenue are incremental.

Citigroup predicts that Nvidia’s stock price may remain volatile for the next two quarters before Blackwell reaches a turning point in annual sales and gross profit margin. As production costs for Hopper and Blackwell rise, most analysts expect Nvidia’s gross profit margin to continue to decline in the coming quarters.

For the second question, Huang Renxun remains optimistic about the future of AI applications, reiterating that global data centers are a trillion dollar opportunity. In Wall Street reviews, Citigroup, Bank of America Merrill Lynch, Goldman Sachs, Morgan Stanley, and others all expressed optimism about the future demand for AI chips.

Unlike the worried market, most Wall Street investment banks are optimistic about Nvidia’s growth prospects, with Citigroup, Bank of America Merrill Lynch, and Goldman Sachs all maintaining buy ratings for Nvidia. Bank of America Merrill Lynch stated that Nvidia has unique growth opportunities and strong execution capabilities, Goldman Sachs has a constructive attitude towards Nvidia’s data center prospects, and Barclays believes that key long-term issues have been resolved.

The following is a summary and commentary from Wall Street on Nvidia’s Q2 financial report and conference call:

Morgan Stanley

Morgan Stanley summarized Nvidia’s financial report and market reaction as the result of a bull market case, but a bear market price action.

According to Shawn Kim, an analyst at Dahmo, “Nvidia’s Q2 performance met expectations, there were no doubts about demand, and the forward guidance was positive.” Overall, its performance was good, but “good alone is not enough,” and “the market’s expectations for Nvidia are too high.

Despite exceeding market expectations in both revenue and guidance, Nvidia’s stock price has experienced a severe negative reaction. Da Mo believes that this negative may also mean that investors have become more cautious and expect a slowdown in the growth of the AI industry, especially after a long period of growth.

Bloomberg News

Bloomberg analyst Ian King summarized:

Nvidia’s quarterly sales were roughly in line with analysts’ expectations, but disappointed the most optimistic investors.

The most significant news is that Nvidia has admitted that there are some issues with the design of the upcoming Blackwell chip.

Blackwell encountered issues during the production process and requires rework. However, this chip will still bring in billions of dollars in revenue in the fourth quarter.

Analysts hoped to obtain more details about the launch of Blackwell’s product line, but Nvidia did not provide them, leading to a further significant drop in the company’s after hours stock price during the conference call.

During the conference call, Huang Renxun remained optimistic about the future of AI applications and stated that the company has only just begun to promote the re equipping of global data centers with its equipment. This is a trillion dollar opportunity.

After the conference call, Huang Renxun stated in an exclusive interview with Bloomberg TV that the supply will continue to improve every quarter, and next year’s supply will have a significant improvement compared to 2024. He said that overall, next year will be a great year.

Citigroup

Citigroup maintains a buy rating on Nvidia and a target price of $150, based on a 35 times earnings per share (EPS) ratio expected for 2025. Analyst Atif Malik of the institution wrote:

Blackwell chip: The management has clearly stated that Blackwell is not expected to be launched in October, only samples. Regarding the mask defects that occurred during the production process of Blackwell, the management mentioned that due to the mask defects, they have delayed the delivery time by several weeks. However, they still expect to generate billions of dollars in revenue in the fourth quarter.

Due to ongoing supply chain constraints, they expect strong demand for Hopper series chips from cloud service providers (CSPs) and enterprises.

Non GAAP gross profit margin: The expected decline in gross profit margin for the third and fourth quarters is mainly due to the increased proportion of higher performance H200 chips and high bandwidth memory (HBM) combinations, which have pushed up GPU production costs.

As for next year, the management expects the gross profit margin to continue to decline in the first quarter (Citigroup estimates over 200 basis points), with Blackwell being a key factor, and the gross profit margin in the second quarter will depend on the situation after Blackwell goes into mass production. Nvidia expects Blackwell’s production to meet their expectations.

AI Network: NVIDIA sees the continued demand for Infiniband (“infinite bandwidth” technology) and plans to develop the next generation of Infiniband products. On the other hand, Nvidia is increasing its Ethernet products by offering many of the features they provide in Infiniband products. In terms of enterprise demand, the management believes there are several key driving factors: AI agents, Co Pilot, and robots.

Citigroup expects that Nvidia’s stock price may maintain range volatility in the next two quarters before Blackwell drives Nvidia’s annual sales and gross profit margin to a turning point. The Consumer Electronics Show (CES) held in January is Nvidia’s next major stock price catalyst.

In addition, as the demand for enterprise AI takes off, the adoption of AI is still in the third/fourth stage, and the demand for data computing will significantly increase by 10-20 times in the long run.

Bank of America Merrill Lynch

Bank of America Merrill Lynch reiterated its buy rating on Nvidia, raising its EPS forecast for fiscal years 2024/25 and 2025/26 by 9% to $2.81/3.90, and raising its target price from $150 to $165.

Analysts such as Vivek Arya from Bank of America Merrill Lynch stated that the fluctuation in Nvidia’s stock price is likely due to the possibility of Blackwell’s delivery being delayed by one quarter.

The agency also expects Nvidia’s gross profit margin to drop to 75% in the third quarter and further to 73% in the fourth quarter as Blackwell costs rise.

Although quarterly performance may fluctuate, Bank of America Merrill Lynch remains optimistic about Nvidia’s long-term growth prospects, stating that Nvidia has unique growth opportunities and strong execution capabilities, thanks to its leading position in the field of generative AI and over 80% market share.

The promotion and application of generative AI technology is currently in its early stages (1-1.5 years), and the investment cycle is expected to last for 3 to 4 years.

Importantly, the next generation of AI models will require 10-20 times more computing power to train (Blackwell’s computing power is only 3-4 times higher than Hooper’s).

AI deployment remains a crucial task for global cloud/enterprise customers, and Nvidia offers the best one-stop model.

Bank of America Merrill Lynch believes that the main factors driving Nvidia’s stock price increase include:

The demand for Hooper series products is strong, and despite being launched for two years, it is expected that demand will be higher in the second half of the year, with Blackwell contributing additional revenue.

The demand of sovereign customers increased, and the order volume increased from high single digit US $billion to low double digit US $billion. The customer composition was diversified, with super large customers accounting for 45% and Internet service companies and corporate customers accounting for 50%.

The demand for AI Ethernet products is strong, and it is expected to become a product line worth billions of dollars.

The significant increase in pre orders, with a year-on-year growth of 149% to $27.8 billion in the second quarter, demonstrates the market’s confidence in Nvidia products.

Goldman Sachs

Goldman Sachs has maintained a buy rating on Nvidia and a target price of $135, with analysts Toshiya Hari and others pointing out:

Although we expect the gross profit rate of Nvidia in the fourth fiscal quarter (the first quarter of natural year 2025) to be less than 70%, and the company’s growing operating expenditure budget will drive the market to re price the gross profit rate expectations in the future fiscal year, we still have a constructive attitude towards the revenue outlook of Nvidia’s data center, which covers cloud services, consumer Internet and enterprise customers, as well as training and reasoning workloads.

On the positive side, regarding Blackweil, the management has confirmed that they have undergone a redesign without any compromise on performance, and it may bring in billions of dollars in revenue in the fourth quarter, not including Hooper’s revenue which is still growing.

In our model, we have lowered our adjusted non GAAP gross profit margin forecast for the 2026/27 fiscal year by 200 basis points/210 basis points. However, due to the increase in data center revenue, we have moderately raised our adjusted non GAAP earnings per share forecast for the 2026/27 fiscal year by 3%/1%.

Barclays

Barclays maintains its overweight rating on Nvidia and a target price of $145, with analysts Tom O’Malley and others stating in a report:

Although the guidance did not meet the most optimistic market expectations, we believe that key long-term issues have been resolved, paving the way for a strong start to the 2025 fiscal year.

We understand that investors may nitpick this financial report from a superficial perspective, but the key issues are moving in a positive direction.

Although the guidance did not exceed the consensus expectation of $2 billion as before, with lower gross profit margins and higher operating expenses, more importantly, Blackwell’s concerns about delays have been resolved, and it is expected that there will be billions of dollars in revenue in the fourth quarter, with Hooper continuing to grow by the end of the year.

Overall, the revenue has clearly maintained continuity and stability, and the company has specifically mentioned that it expects to continue to grow significantly next year.

The stock market’s response seems to be more related to changes in investment themes rather than the more conservative guidance we believe during product transitions. We will increase our holdings of (Nvidia) when the stock price falls.

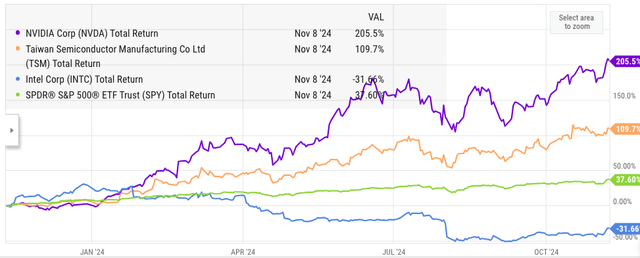

TSMC (NYSE:TSM) continues to deliver strong results, with sentiment on Wall Street improving despite headwinds such as the recent chip export ban.Year-to-date, TSMC stocks have returned 109% totally, compared to 37% for the S&P 500. In addition to the solid performance of recent earnings, TSMC also reported good news from its Arizona plant. According to Bloomberg, the output of the Arizona plant has already exceeded the output of similar factories in Taiwan. This should help the company gain strong support from the U.S. government. On the other hand, Intel faces a number of challenges and is currently delaying or canceling the construction of several factories in Germany, Poland and other regions.

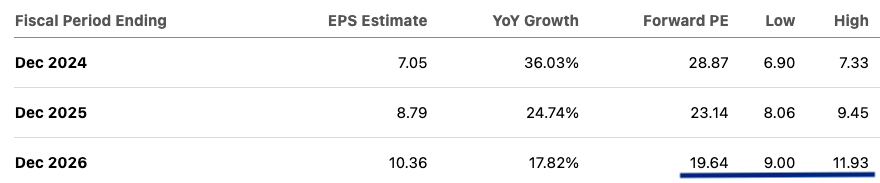

TSMC is gaining momentum, and its EPS growth forecast for the next two years is quite strong.EPS for the fiscal year ending December 2026 is forecast at $10.36 and the forward price-to-earnings ratio is 19.6. When we look at the company’s moat and its role as a major supplier to many big tech companies, the figure is fairly modest.

TSMC beat EPS and revenue expectations in this earnings report. Nearly 70% of total revenue comes from the 7nm node or lower, demonstrating the company’s rapid progress over the past few quarters. It is now the exclusive supplier to several major big tech companies, making it an integral part of the supply chain.

We’ve heard of hyperscalers investing huge capital expenditures in AI chips. Most of these chips are manufactured by TSMC, which has shown strong revenue growth potential due to strong demand for AI.

So far this year, TSMC’s stock has led the way with a total return of 109%. With the exception of Nvidia, this is one of the stocks with the highest returns, far outperforming many other competitors.

Intel wants to invest heavily in the foundry space to gain market share. Over the past two years, the company has invested nearly $25 billion a year to build different plants. However, Intel is now facing significant headwinds due to Wall Street’s concerns about the company’s ability to perform well in the near term. This has led to a sharp year-to-date correction in Intel’s stock price. Intel has delayed the construction of many new factories in Germany, Poland and elsewhere. Intel continues to face production challenges at lower nodes and plans to slash capital spending to calm investor jitters. Samsung’s chip production capacity is also challenged and it has ceded market share to TSMC.

Intel’s weakening competition will improve TSMC’s market sentiment, and since the company controls a huge market share, it is likely to see higher profit margins for the company in the coming quarters.Nvidia’s stock has been performing better than TSMC so far this year, but analysts believe TSMC has a better moat. Nvidia faces competition from AMD and other tech giants who are building their own AI chips. Most chip manufacturing is done by TSMC. There is a good chance that Nvidia will lose market share in the AI space, but TSMC’s total revenue may not be negatively impacted, as TSMC is the primary supplier of manufacturing facilities to most of its competitors.

TSMC’s EPS growth momentum continues to be strong. For the fiscal year ending December 2025, EPS is expected to be $8.79 and the stock is trading at an expected price-to-earnings ratio of 23.14. For the fiscal year ending December 2026, EPS is expected to be $10.36 and the stock is trading at an expected price-to-earnings ratio of just $19.64. In terms of growth runways, moats, and operational efficiencies to deliver good earnings, the numbers are quite modest.

TSMC’s earnings profile is stable.As we can see from the chart above, for the fiscal year ending December 2026, the EPS low forecast is $9, while the EPS high forecast is $11.93, which is 33% higher than the low forecast. This is a fairly narrow range for expected EPS forecasts, which indicates confidence in future earnings growth. Many other big tech companies, such as Nvidia, also have large differences in their expected earnings per share forecasts.

For the fiscal year ending January 2027, Nvidia’s high EPS forecast is 4 times higher than its low EPS forecast. This difference is due to expectations of the company’s market share, margins, and revenue growth. In terms of the consensus EPS forecast for the fiscal year ending January 2027, Nvidia shares are trading at 30 times. This is significantly higher than TSMC’s expected price-to-earnings ratio of less than 20 for the fiscal year ending December 2026.

As a result, TSMC may be a better investment for investors looking for stable EPS growth momentum and more certain future EPS forecasts.

TSMC has achieved strong results in the financial report and continues to show good growth momentum. The company also announced good production at its Arizona facility, which will help it gain more support from the U.S. government. On the other hand, competitors such as Intel and Samsung are facing significant challenges and have announced the cancellation or postponement of the construction of new factories.

TSMC has a better moat than many other big tech companies because it provides manufacturing facilities for all major players. Any change in market share in the field of artificial intelligence or other businesses will not affect the demand for TSMC facilities. We can see this clearly in the narrow forward EPS range for many analysts. In the next 2 fiscal years, TSMC’s forward P/E ratio is less than 20, while Nvidia’s P/E ratio is close to 30. Lower valuation multiples and the certainty of forward EPS forecasts make TSMC a good choice for investors.

This year, Tesla CEO Elon Musk’s social media activities on X have significantly increased. The latest data shows that Musk has posted 13000 posts this year, which is equivalent to an average of 61 posts per day.

By contrast, in 2019, Musk released an average of only 9 posts per day. In addition, the content of these posts has also shifted more towards politics, especially since July this year, when they explicitly expressed support for former President Donald Trump.

As of the end of July, the number of posts posted by Musk this year is almost the same as the total of the previous year.

According to an analysis of nearly 42000 social media exchanges between 2019 and the end of July this year, Musk’s posts are increasingly focused on political and social issues. This year, the number of exchanges (posts) containing political terms is approximately 230 times that of 2019.

In fact, since the outbreak of the pandemic, Musk’s posts have become increasingly politically charged. Musk’s shift towards political content is not without controversy. The report states that his posts involve sensitive political and social issues, sometimes amplifying provocative or conspiratorial content.

Musk’s increased political involvement coincides with the challenges facing his social media platform X. Since Musk’s acquisition, the platform’s revenue has plummeted by 84%. This has raised concerns among Tesla investors that Musk may liquidate more Tesla stocks to fill the financial gap, which could damage Tesla’s value.

Recently, Musk conducted a public opinion poll on X to assess the political affiliation of his 196 million fans. This survey received 1.6 million responses, of which 49.4% identified themselves as Republicans, 35.2% as independents, and 15.3% as Democrats.

There are also reports that the Royal Society in the UK is facing pressure to dismiss Musk due to concerns over his controversial remarks.

Just now, the United States released a set of heavyweight economic data.

The construction of new houses in July showed an annualized total of 1.238 million households, with an expected 1.33 million households. The previous value was revised from 1.353 million households to 1.329 million households. The total number of construction permits in the United States in July was 1.396 million, with an expected 1.429 million, and the previous value was revised from 1.446 million to 1.446 million.

In addition, the August consumer survey conducted by the University of Michigan in the United States was released.

Among them, the initial expectation for the one-year inflation rate in the United States in August is 2.9%, with an expectation of 2.90%, compared to the previous value of 2.90%. The initial value of the University of Michigan Consumer Confidence Index for August in the United States is 67.8, with an expected value of 66.9, compared to the previous value of 66.4. The initial value of the University of Michigan Current Situation Index for August in the United States is 60.9, with an expected value of 63.1, compared to the previous value of 62.7. The initial expected inflation rate for the five to ten year period in the United States for August is 3%, with an expectation of 2.90%, compared to the previous value of 3.00%. The initial value of the University of Michigan Expectations Index for August in the United States is 72.1, with an expectation of 68.5, compared to the previous value of 68.8.

Regarding the interpretation of the above data, Joanne Hsu, Director of Consumer Research at the University of Michigan, stated that with the development of this month’s election becoming headline news, after Harris replaced Biden as the Democratic presidential candidate, the sentiment of Democrats has risen by 6%. The sentiment of Republicans, on the other hand, has decreased by 5% this month. The sentiment of neutral non partisan individuals has risen by 3%.

He stated that the survey showed that 41% of consumers believe Harris is a better candidate in terms of the economy, and 38% chose Trump. Overall, expectations for personal financial condition and five-year economic outlook have increased to the highest level in four months, which is consistent with the fact that election developments may affect future expectations but are unlikely to change current assessments. However, some consumers point out that if their expectations for the election are not met, their expected trajectory for the economy will be completely different. Therefore, as the presidential election becomes a bigger focus, consumer expectations may change.

Powell will speak out

Data from the US Department of Labor on Wednesday showed that the Consumer Price Index (CPI) rose 2.9% year-on-year in July, the lowest level since 2021.

Some analysts believe that the focus of discussion at the Federal Reserve’s September meeting will be on whether to follow the traditional 0.25 percentage point rate cut or increase the magnitude by 0.5 percentage points.

The next event to focus on is Federal Reserve Chairman Powell’s speech on the US economic outlook next Friday (August 23) at 10:00 Eastern Time. At that time, Powell will attend the Jackson Hole Global Central Bank Annual Meeting hosted by the Kansas City Fed (August 22-24).

According to data from JPMorgan, three-quarters of global arbitrage trades have been closed, and recent selling has wiped out this year’s gains. Morgan Stanley’s quantitative strategists Antonin Delair, Meera Chandan, and Kunj Padh stated in a report that the return rates of the 10 country group, emerging markets, and global arbitrage trading baskets tracked by the bank have fallen by about 10% since May. This round of decline has wiped out the returns so far this year and significantly reduced the profits accumulated since the end of 2022.

Morgan Stanley’s quantitative strategist stated, “The spot portion of the global arbitrage trading basket indicates that 75% of arbitrage trades have been cancelled.” They reiterated that the time for arbitrage trades in the 10 country group is running out.

It is reported that global stock markets experienced Black Monday, and the lifting of yen arbitrage trading is considered the core reason for the market collapse. Arbitrage trading refers to investors borrowing currencies from countries with lower interest rates, such as Japan, to provide funds for purchasing high-yield assets elsewhere. Over the past week, global market volatility has intensified and arbitrage trading has been hit hard due to concerns about the Federal Reserve’s rapid interest rate cuts and the Bank of Japan’s interest rate hikes exceeding expectations.

The recent selling speed is twice the usual rate of decline in arbitrage trading, and strategists suggest that the chance of a rebound in August may be small because “the central bank’s schedule during this period is not much, and volatility has begun to cool down

However, they emphasized that the global arbitrage trading strategy “did not provide attractive risk return”. Since the high point in 2023, the yield of a basket of trades has dropped significantly, which is not enough to compensate for the risk of holding high beta assets in emerging markets during the US election period and further repricing low yield bonds when US yields decline

Technical pullback in US stock market

After several months of sustained gains, the strong rally of the US stock market seems to have come to an abrupt end in July: since the S&P 500 index hit a historic high on July 16th, the index has begun to oscillate and decline, falling for four consecutive weeks on the weekly candlestick chart, with a cumulative decline of over 8%. The cumulative decline of the Nasdaq 100 index is even more than 10%.

On Wednesday Eastern Time, Savita Subramanian, head of equity and quantitative strategy at Bank of America, reassured the market that the recent sharp sell-off in US stocks is just a “common technical adjustment” and is unlikely to turn into a comprehensive bear market, with no signs of the stock market peaking yet.

Behind the decline in the US stock market, there are multiple factors driving it: the explosive July non farm payroll report in the United States, the withdrawal from yen arbitrage trading, and increased market concerns about a US economic recession.

Sabramanian believes that the performance of the US stock market in the past few weeks is not a trend of the stock market plummeting after reaching its peak, but more likely a typical adjustment that occurs on average every year. He pointed out that from the history of the US stock market, market corrections are very common.

A pullback of over 5% is common, occurring on average more than three times a year since 1930 (this is the second time this year after April). Larger adjustments are less frequent, but still common, occurring on average once a year of over 10% (the most recent being in the fall of 2023), “Subramanian wrote in the report.

Introduction to the basic information and business of Simon Property Group, Inc. (SPG.N) Company.

Company Overview:

Company Name: Simon Property Group (SPG.N) is a real estate investment trust (REIT) headquartered in the United States.

Stock Ticker: SPG (Listed on the New York Stock Exchange)

Business Scope:

Shopping Centers: Simon Property Group is one of the world’s largest shopping center operators. The company owns and manages shopping centers of various sizes and types, including indoor shopping centers, outlet centers, and large shopping complexes.

Tenants and Partners: The company has established partnerships with numerous retailers, restaurants, and other commercial partners to provide various leasing services for its shopping centers.

Geographical Distribution: Simon Property Group’s shopping centers are mainly located throughout the United States, including in cities, suburbs, and tourist destinations. Additionally, the company seeks investment and business opportunities globally.

Outlet Centers: Simon Property Group is renowned for its outlet centers, which typically offer discounted retail of branded goods. This attracts consumers seeking a discount shopping experience to a certain extent.

REIT Structure: As a real estate investment trust, Simon Property Group operates under a special legal structure that requires the distribution of a significant portion of income to shareholders and compliance with specific tax regulations.

In which areas does the company hold a leading global position, and what are the key success factors?

Global largest shopping center operator: Simon Property Group is one of the largest shopping center operators globally, owning and managing shopping centers of various sizes and types. This gives the company extensive influence and market share in the retail real estate sector.

Diversified real estate investment portfolio: The company holds a diversified real estate investment portfolio in different geographical locations, cities, and suburbs. This diversity helps to reduce risks, enabling it to better adapt to the varying demands and trends of different markets.

Successful model of outlet centers: Simon Property Group has successfully promoted the concept of discount retail through its outlet centers. These centers are typically located on the outskirts of cities, offering discounted retail of well-known brand products, attracting consumers seeking more attractive prices.

Positive brand partnerships: The company has established positive relationships with numerous retailers, dining establishments, and other commercial partners. Collaborating with globally renowned brands helps attract more tenants and enhance the appeal of shopping centers.

Prime commercial and retail locations: Simon Property Group’s shopping centers are usually situated in prime locations in cities and commercial hubs, providing tenants with unique business opportunities and foot traffic. This superior location is one of the key factors contributing to the company’s success.

Asset management and operational expertise: Simon Property Group possesses extensive asset management and operational experience, enabling it to efficiently manage large-scale shopping centers and real estate investment portfolios.

Analysis of the company’s main strategic transformations, core driving factors, and key events since its establishment.

Early development and expansion: Simon Property Group was founded in 1960, initially focusing on the development of shopping centers. In the 1970s and 1980s, the company experienced rapid expansion by acquiring and developing shopping centers, establishing its foundation in the real estate industry.

Outlet Center Strategy: In the 1990s, the company introduced the concept of outlet centers, which feature discounted retail offerings from well-known brands. This strategic transformation successfully met consumers’ demand for discount shopping and became an important business for Simon Property Group.

Globalization and international expansion: Over time, Simon Property Group gradually expanded globally, seeking opportunities in international markets. This included investing in and developing shopping centers in various countries to expand its global influence.

Digitalization and technological innovation: With the digital transformation of the retail industry, Simon Property Group took measures to integrate technological innovations. This involved collaborations with online retailers, digital payment options, and the application of augmented reality (AR) technology to enhance the attractiveness of shopping centers.

Adapting to retail industry changes: Simon Property Group implemented strategies to address changes in the retail industry, such as adding entertainment, dining, and experiential elements to shopping centers to increase customer dwell time and promote social interactions.

Asset management and optimization: The company has always focused on effective asset management and optimization, actively managing its shopping centers and real estate investment portfolio to maximize investment returns.

Key events and investment transactions: Throughout its development, Simon Property Group has experienced a series of key events and investment transactions, including acquisitions, joint ventures, and sales of various types of real estate assets to adjust its investment portfolio and seek better business opportunities.

Since its establishment, the company has had various CEOs and their major contributions during their tenures.

Melvin Simon (Founder, established in 1960): Melvin Simon was one of the company’s founders. He laid the foundation for the company by developing shopping centers. Melvin Simon’s leadership led the company to significant achievements in the shopping center industry.

Herbert Simon (Melvin Simon’s brother, 1960 – 2007): Herbert Simon, Melvin Simon’s brother, co-founded the company with Melvin. Under his leadership, the company underwent multiple expansions, becoming one of the world’s largest shopping center operators.

David Simon (2007-present): David Simon, Herbert Simon’s son, took over as CEO in 2007 and continued to drive the company’s success. Under David Simon’s leadership, the company further strengthened its position in the shopping center industry in the United States and globally. He has been dedicated to adapting to changes in the retail industry by introducing entertainment and dining elements to enhance the appeal of shopping centers.

Future Development Prospects of the Company

Retail Industry Trends: Focus on changes and trends in the retail industry, especially the impact of e-commerce and online retail on physical retail. The company may take measures to adapt to these changes, such as enhancing the shopping center experience, digitalization, and technological innovation.

Geographical Expansion: The company may plan to expand into new geographical regions to further consolidate its global real estate investment portfolio.

Strategic Partnerships: The company may seek to establish strategic partnerships with other businesses to expand operations or drive innovation.

Sustainability and Social Responsibility: The company may focus on sustainability and social responsibility, taking measures to reduce environmental impact and play a more active role in society.

In this era of rapid change, AI technology is evolving at an unprecedented rate, bringing a wide range of opportunities. AI Daily is committed to mining and analyzing the latest AI concept stock companies and market trends, providing you with in-depth industry insights and value analysis.

AI News

1.U.S. stocks rose across the board on Monday as the effects of Trump’s victory continued, as investors awaited key economic data and corporate earnings later in the week.

At the close, the Dow rose 304.14 points, or 0.69%, to 44,293.13, the Nasdaq rose 0.06% to 19,298.76, and the S&P 500 rose 0.10% to 6,001.35. The small-cap Russell 2000 rose 1.5% to its highest level since November, with small and medium-sized businesses expected to be the main beneficiaries of President-elect Trump’s proposed tax cuts and looser regulatory environment.

In terms of individual stocks, Tesla rose 9.0%, surpassing TSMC in market capitalization to rank seventh in U.S. stocks. Wedbush Securities said in a note to clients that the electric vehicle maker’s AI business development could receive more support from Trump.

2.At the Baidu World Conference on November 12, Baidu CEO Robin Li revealed that the current average daily call volume of Baidu’s Wenxin model exceeds 1.5 billion, an increase of 7.5 times in half a year. He pointed out that after the basic model capabilities are ready, it will usher in the star shining moment of AI applications. There are two application directions for AI applications, agents and industrial applications, and intelligence will be the most mainstream form of AI applications, which is about to usher in its flashpoint.

In Robin Li’s view, the current agent is like a website in the PC era, or a self-media account in the mobile era, the difference is that the agent is more intelligent, and may become a new carrier of content information and services in the AI native era. He analyzed that this is mainly because the threshold for agents is low enough for anyone to get started, and on the other hand, the ceiling is high enough to make very powerful applications.

3.Japanese Prime Minister Shigeru Ishiba unveiled a $65 billion plan to boost the country’s chip and artificial intelligence (AI) industries through subsidies and other financial incentives.

Shigeru said the government would not issue deficit bonds to fund plans to support the chip industry. According to the draft, the government expects the economic impact of these measures to reach about 160 trillion yen.

4.Nvidia shares have nearly tripled this year, and Wall Street analysts are extremely bullish on the chipmaker. But Terry Smith disagreed.

The fund manager, who has been dubbed the British buffett by the British press, is skeptical. He said the world’s largest stock lacks a predictable profit stream and an excellent track record of high returns on capital. Smith is shunning the stock, although he acknowledges that it would weaken the performance of his portfolio.

5.On Monday morning, November 11, Eastern time, Edgewater Research, an investment company, sent a notice to investors that Monolithic Power (referred to as MPWR, Xinyuan Systems) may have problems with the voltage regulation module/power management chip produced for Nvidia’s Blackwell chips, which may cause the company to be unable to supply Nvidia’s Blackwell graphics cards, and the supply share will be cut or even completely lost.

They believe that Renesas could take over the B200 project and Infineon could take over the GB200 project, as both companies have been receiving orders urgently in recent weeks. Edgewater Research also said it had heard that Nvidia had canceled all unconfirmed orders for the core source system.

The news caused the share price of Xinyuan Systems to fall nearly 25% in intraday trading on Monday, the largest intraday decline since 2005.

Institutions look at AI

1.Guotai Junan Research Report pointed out that the Robotaxi industry has ushered in a key technological breakthrough. At the end of the 20th century and the beginning of the 21st century, the concept of the Robotaxi industry emerged; In the 2010s, the Robotaxi industry ushered in a key technological breakthrough; In the 2020s, the Robotaxi industry gradually matured. There are many challenges in the future commercialization process.

Robotaxi faces many challenges in the commercialization process, including technical challenges, cost challenges, and regulatory and policy challenges. These challenges are not only the bottleneck of the industry’s development, but also the driving force of technological progress and business model innovation. 1) The Robotaxi industry chain has completed self-production and self-development. Upstream: Autonomy of core technologies. It mainly involves two categories: perception systems and algorithms and software. The perceptron is the eye of the Robotaxi, the intelligent driving chip is the brain of the Robotaxi, and the algorithm is the nerve of the Robotaxi. 2) Robotaxi will continue to advance in technology and business model in the future. Technological advancements: The evolution of autonomous driving technology will provide the application of new models (self-organizing neural networks; GOD model) business model: In the future, the charging model and profit strategy will be further adjusted according to market demand, focusing on market expansion and regional coverage of possible market participants in the future: Huawei, Xpeng, Celis and other OEMs, as well as Tesla’s Cybercab plan. New entrants have more flexible strategic layouts and advantages.

The Big Seven Daily

[Monolithic Power Systems shares plummet as Blackwell’s distribution was ‘at risk’]

Monolithic Power Systems (NASDAQ:MPWR) plunged 14% in premarket trading on Monday as investment firm Edgewater Research said the company’s (NASDAQ:MPWR) configuration of Nvidia’s (NASDAQ:MPDA) Blackwell series GPUs was “at risk.”

“It appears that performance issues with MPWR (voltage regulator module/power management IC) could severely limit or eliminate MPWR’s quota at Blackwell, with Renesas receiving a £200 quota and Infineon receiving a £200 quota as both companies have received urgent orders in recent weeks,” the company’s analysts wrote in a note to customers. The Japanese company Renesas and the German company Infineon (OTCQX: IFNNF) (OTCQX: IFNNY) are mentioned.

The analyst added that the root cause of the Monolithic power management IC issue is “not yet known”, but feedback suggests that it may be related to a product failure that was identified earlier this year at the Blackwell SKU that consumed more than 700 watts. For analysts, this means that Monolithic’s B200 (1,000 watts) and GB200 (1,200 watts) SKUs are “limited or none” in stock, and the company will likely only ship for the B300A (700 watts).

“We’ve heard that NVDA will be transferring confirmed orders to MPWR in the coming quarters, but we’ve heard that NVDA has eliminated half of MPWR’s backlog and cut all unconfirmed orders,” the analyst explained. “It seems that Renesas’ Hopper allocation could grow to 50% in the first or second quarter of 2025, compared to about 15% in the fourth quarter of 2024. We are not aware of IFX’s plans to qualify for Hopper. It sounds like NVDA Engineering has lost faith in MPWR, and they have decided to make Renesas and IFX their two main suppliers. ”

Analysts also noted that Monolithic’s solution to the hopper problem was seen as a “stopgap measure” by multiple supply chain partners rather than a true solution to the underlying problem.

“We believe this will pose significant downside risks to MPWR’s enterprise data division in 2025 and will also pose significant risk to the share price as investors are more focused on MPWR’s AI performance, which currently masks the company’s strong performance in other sectors,” the analysts added. ”

Artificial intelligence giant SMCI. US saw its stock price drop 20.14% on Wednesday, August 7th, to close at $492.70 due to lower than expected performance. From its high of $1229 five months ago, its stock price has fallen by 60%!

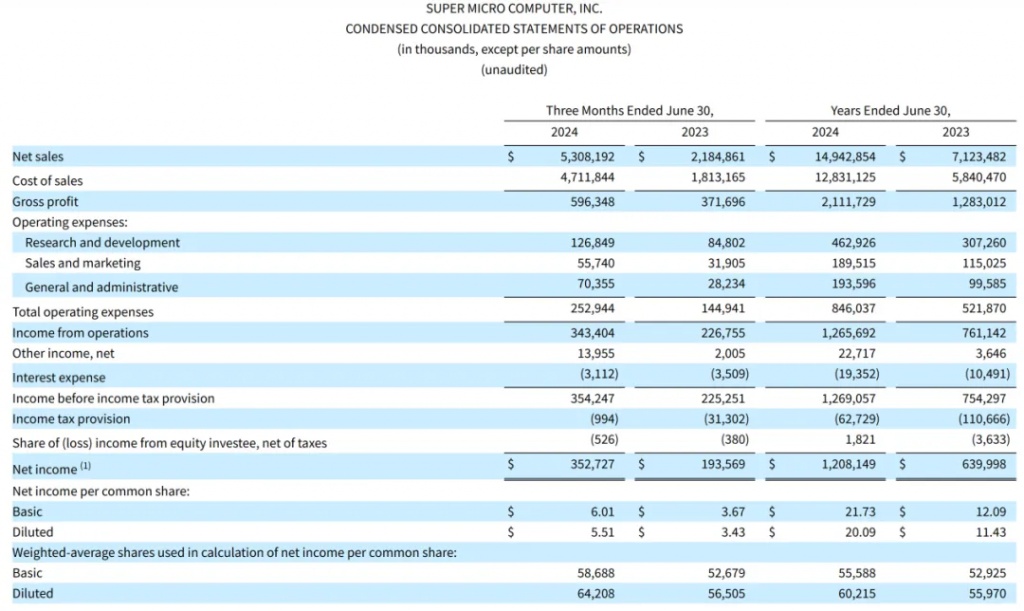

According to the latest financial report released by Supermicro Computer, the company’s adjusted earnings per share for the fourth quarter of the 2024 fiscal year ended June 30 were $6.25, far below analysts’ expectations of $8.07; The gross profit margin was 11.2%, far lower than the 15.5% in the previous quarter and below analysts’ expectations of 14.1%.

Supermicro Computer achieved a revenue of 5.308 billion US dollars in the second quarter, a year-on-year increase of 142.95%, roughly in line with market expectations of 5.3 billion US dollars; Non accounting standard diluted earnings per share increased by 78.06% year-on-year to $6.25, lower than market expectations of $8.07.

For the fiscal year ending June 30, 2024, Supermicro Computer’s annual revenue was $14.943 billion, an increase of 109.77% year-on-year. Non accounting standard diluted earnings per share increased by 87.04% year-on-year to $22.09.

Although the company’s revenue continues to grow, its profitability has declined. In the second quarter, the gross profit margin of Supermicro Computer decreased from 17.01% in the same period last year to 11.23%; Without considering the impact of stock for salary, the non accounting standard gross profit margin also decreased from 17.06% in the same period last year to 11.29%.

The management stated that the decrease in gross profit margin is mainly due to differences in product and customer mix. The company is now focused on winning strategic new designs at competitive prices, as well as the initial cost increase caused by the new DLC AI GPU cluster in the production ramp up. In the future, innovative platforms based on multiple new technologies will be introduced from strategic partners, and the production efficiency of their DLC solutions will be improved.